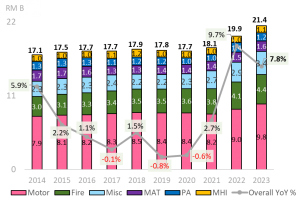

Kuala Lumpur, 1 April 2024 – The general insurance industry recorded an increase in gross written premiums of 7.8% to RM21.4 billion for 2023 compared to the previous year. Despite the positive trajectory, the underwriting profit experienced a contraction of 26%, settling at RM1.16 billion. This decline is largely due to contraction in profitability for Motor and Fire lines of business. Specifically, the loss for Motor portfolio further deteriorated by RM153 million compared to the previous year, due to deterioration of Motor claim experience edging closer to pre-pandemic levels due to inflationary cost pressures on vehicle spare parts [1] and an increase in road accidents rate.

According to AM Best, over the near to medium term, premium growth will be supported by sustained economic recovery and increased insurance penetration due to government initiatives, greater awareness of the importance of insurance protection and the growing demand for digital insurance [3].

Motor and Fire lines of business continue to dominate as top premium contributors

Motor retained its position as the largest line of business at 45% share of total premium. Despite a commendable 9% growth in gross written premiums, reaching RM9.8 billion in 2023, Motor insurance experienced an underwriting loss of RM156 million with net claims incurred ratio at 66.7%, reverting towards pre-pandemic levels.

Meanwhile, the Fire line of business, which is the second largest line of business accounting for 21% share of the total premium, recorded an 8% increase in premium in 2023, totalling RM4.4 billion compared to 2022. However, the Fire portfolio experienced a decline in underwriting profit with the combined ratio approaching 69.5%. This decline is attributed to increasingly volatile weather events including various flood events in 2023, coupled with rising reinsurance costs which will continue to exert pressure on underwriting margins [2][3].

AM Best [3] also notes that since implementation of the phased de-tariffication on these lines of business, Malaysia’s non-life segment has seen an uptick in pricing competition, which is likely to pressure pricing over the near to medium term; however, in the long term, de-tariffication is seen as helping to strengthen the sustainability of the insurance industry.

The Marine Aviation and Transit (MAT) classes of insurance, which accounts for a 7% share of the total premium, recorded a deceleration in year-on-year premium growth, setting at 3% in 2023 as compared to 6% in 2022. Subsequently, the premiums for Miscellaneous classes of insurance, constituting a 16% share of the total premium displayed an upwards trend with a robust year-on-year premium growth of 18% in 2023. The significant growth in Miscellaneous classes was mainly driven by Construction All Risk (CAR) & Engineering business whereby the premium growth was driven by the robust construction sector, supported by the revival and acceleration of mega infrastructure projects [4].

Personal Accident (PA) line of business, at 6% share of the total premium, witnessed an anticipated drop in premium by 16.2% year-on-year owing to the ending of the successful Perlindungan Tenang Voucher (PTV) programme in 2022. An improvement in the tourism industry may benefit the travel industry segment as per TA research [5] and potentially bolster the PA line of business.

Medical and Health Insurance (MHI) demonstrate a significant increase in year-on-year premium growth at 10.4% in 2023, highest year-on-year premium growth in a decade.

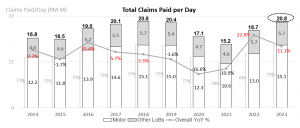

Claims payout by insurance industry rises to RM21 million per day in 2023

The general insurance industry settled on average RM21 million daily on total insurance claims in 2023, an increase of 11% YoY. Over the past decade (2014-2023), Motor daily claims payout represented majority of total claims averaging at RM13.4 million per day, constituting 72% of total payout. In 2023, Motor daily claims payout increased to RM15.1 million per day, the highest payout in the recent 5 years.

[1] MalaysianRe, “Asean Insurance Pulse 2023”, 5/12/23.

(www.malaysian-re.com.my/api/uploads/ASEAN_Insurance_Pulse_2023_113442a317.pdf), 5/12/2023.

[2] AHA Centre, “FLASH UPDATE: No. 01 – Flooding, Landslides, and Storms in Peninsular Malaysia and Southern Thailand – 27 December 2023”, 27/12/23

(https://ahacentre.org/flash-update/flash-update-no-01-flooding-landslides-and-storms-in-peninsular-malaysia-and-southern-thailand-27-december-2023/#:~:text=IMPACTS%3A%20As%20of%2027%20Dec,displaced%20in%20133%20evacuation%20centres.)

[3] AM Best Market Segment Report – Malaysia Non-Life Insurance, 19/12/23 (https://news.ambest.com/pr/PressContent.aspx?refnum=34241&altsrc=2)

[4] Bernama, “Revival of mega infrastructure projects sparks construction sector growth, sustainability at work”, 30/11/23

[5] The Star news – Resilient demand to spur insurance industry, 28/12/2023. (www.thestar.com.my/business/business-news/2023/12/28/resilient-demand-to-spur-insurance-industry

~ END ~

…………………………………………………………………………………………….

About General Insurance Association of Malaysia (PIAM)

PIAM is the national trade association of all licensed direct and reinsurance companies for general insurance in Malaysia. Currently, PIAM has 23 member companies. More information on PIAM can be obtained from its website: www.piam.org.my.

Media Relations Contact:

Ms. Susanna G. Simon

Manager, Consumer Education, PR & Corporate Communications

Persatuan Insurans Am Malaysia (PIAM)

Tel : +603-2274 7399

Fax : +603-2274 5910

E-mail : susanna.simon@piam.org.my