Phased Liberalisation, Covid-19 and the Motor Insurance Industry

Kuala Lumpur, 23 March 2021 – As the global pandemic enters its second year with uncertainty persisting on the extent to which it will continue to affect daily life, it is opportune for Persatuan Insurans Am Malaysia (PIAM) to provide a commentary and an update of its impacts on the motor insurance industry in Malaysia. In particular, we wish to address prevailing perceptions on the status of ‘phased liberalisation’ on motor tariff and whether the motor insurance industry can be accurately described as an open market with total freedom in pricing.

Phased Liberalisation – New Products and Policy Renewals on Existing Policies

During the phased liberalisation period which started on 1 July 2016, in order to drive product innovation and competition, insurers are allowed to introduce new motor products to better serve the needs of consumers and price them according to insurers’ respective risk pricing models subject to parameters of +/- 10% from the original tariff rates as at 30 June 2016 [1]. The limitation thresholds are meant to cushion the impact of any sudden and significant changes in premium with potential adverse impact on consumers. Any deviation from the aforementioned threshold will require the approval of the industry regulator BNM.

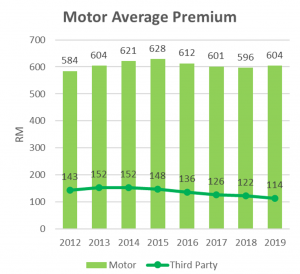

As the graph below shows, average premium has been broadly level since 2016. Average premium in real terms will be lower after accounting for inflation over the same period. Third Party motor insurance average premium decreased by -16% over the same period to 2019 that would have benefited B40 consumers in general.

Source : Data from ISM. Average Premium is based on experience of general insurance conventional business.

PIAM hopes the above clarifies to the motoring public and other stakeholders that while the process initiated for the gradual removal of requirements under the motor tariff has begun, pricing continues to be regulated by the industry regulator. It is important to note that PIAM is not involved in the pricing decisions of its members. Going forward, the industry eagerly anticipates further liberalisation and looks forward to working with BNM on the eventual opening up of the motor market.

Impact of the Pandemic on the Motor Insurance Industry

Motor business has not been precluded from the impact of the pandemic due to weak consumer demand and suspension of economic activity due to the lockdown restrictions caused by the pandemic. Amidst this crisis, consumers have become conscious of their expenditure on purchasing of motor vehicles, thus directly affecting the motor insurance sector. According to the Malaysian Automotive Association (MAA), Total Industry Volume (sales of new passenger and commercial vehicles) registered in 2020 was 529,434 units, a decrease of -12.4% compared to 2019. Gross Direct Premium for Motor insurance fell by 0.21% in 2020 when compared to 2019.

Compounding the impact on demand, as was consistent with other sectors of the Malaysian economy, were rising costs of business operations during the various stages of Movement Control Order (MCO). General insurers worked to ensure minimal disruptions to critical business operations such as new and renewal policies processing, customer service and claims management. A system was created for adjusters to conduct virtual surveys of accident cars so that insurance repairs can proceed as smoothly as possible under MCO conditions. In summary, the general insurance industry had strived to minimise the impact in terms of customers’ experience and delivery of claims services despite the challenging year that was.

Motor business has not been a profitable line of business for many years. Generally, there has been no increase in motor insurance premiums due to the tariff even when motor portfolio was registering losses. In the years where motor loss ratios were high, motor premiums were cross subsidized by other better performing insurance products thus balancing the sustainability of the insurance industry with the important socioeconomic function of meeting consumers’ need for motor insurance.

According to Bukit Aman Traffic Investigation and Enforcement Department (JSPT) the number of road accidents reported in 2020 reduced by -26.3% to 418,237 accidents compared to 567,516 in 2019 [2], largely owing to the MCO. As a result, the Combined Ratio for motor insurance improved by 6.0 percentage points to 98.3% in 2020 from the previous year. Whilst this is a welcome development in terms of a reduction in deaths and injuries, it is unlikely to change the underlying trend unless there is a radical change in both driving habits and enforcement by the authorities. In future, PIAM believes that full liberalization will lead to fairer pricing that will benefit safe drivers and lead to more product innovation, technologically-driven consumer solutions and a better overall consumer experience.

Pandemic Initiatives

The general insurance industry was a contributor to the RM8 million Covid Test Fund (MyCTF) for medical insurance policyholders. MyCTF initiative was created to support the Ministry of Health’s effort to conduct more Covid-19 tests as part of public health measures. Qualified claimants who need financial help to test for Covid-19 are able to seek reimbursement of up to RM300. In December 2020, MyCTF broadened its reimbursement criteria to include claims from asymptomatic patients and hospital admissions.

About General Insurance Association of Malaysia (PIAM)

PIAM is the national trade association of all licensed direct and reinsurance companies for general insurance in Malaysia. Currently, PIAM has 26 member companies. More information on PIAM can be obtained from its website: www.piam.org.my.

Media Relations Contact:

(Ms) Siti Zubaidah Binti Zakaria

Senior Manager, Corporate Communications, PIAM

Tel : +603-2274 7399 x 25 / +60199662717

Fax : +603-2274 5910

E-mail : idazakaria@piam.org.my

Cik Syafa Salihinn

Executive, Corporate Communications, PIAM

Tel : +603-2274 7399 x 34

Fax : +603-2274 5910

E-mail : corpcomms@piam.org.my