Insurance Data

Below are key facts and figures that illustrate how our members are safeguarding Malaysians and their property against emerging and evolving risks.

This data highlights the vital role of general insurance in providing final security and resilience across the nation.

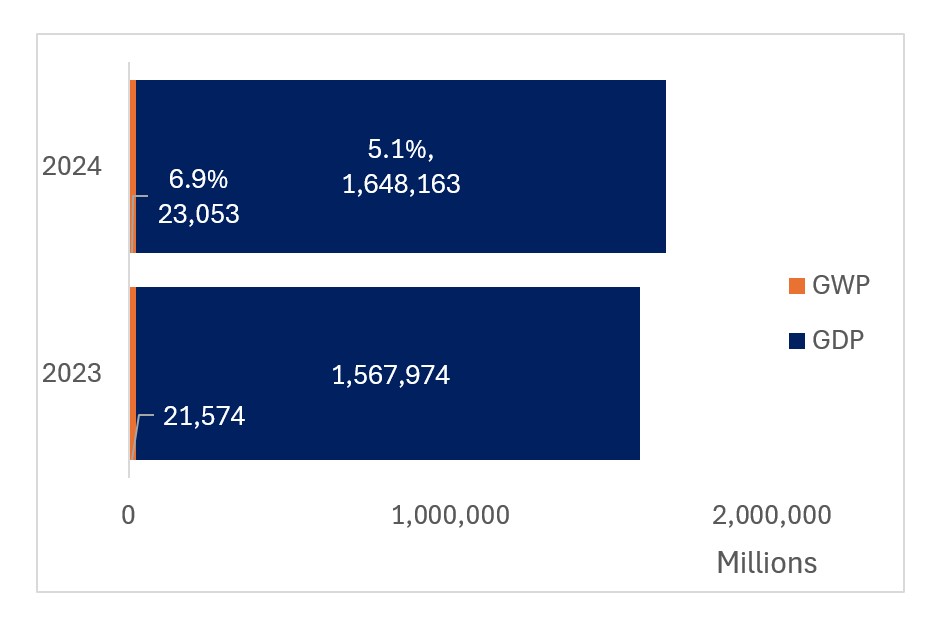

The performance of the General Insurance Operators is intrinsically connected to the nation's Gross Domestic Product (GDP) growth. The industry's resilience has been evident in recent years, as Gross Written Premium (GWP) has consistently grown in step with national economic indicators, even amidst economic shifts.

The resilience of both Malaysia’s economy and the General Insurance (GI) industry continued in 2023 and 2024, both demonstrating positive year-on-year growth in Gross Domestic Product (GDP) and Gross Written Premium (GWP).

In 2024, GWP growth eased slightly to 6.9%, while the overall economy experienced a stronger growth, with GDP rising to 5.1%. Despite the narrowing growth rate compared to the previous year, the general insurance sector maintained its momentum, with GWP growth once again outpacing economic growth – a testament to the industry’s continued relevance and adaptability in a shifting economic landscape.

(Source: GDP – Malaysia’s National Statistics Organisation, as of Feb. 2025; GWP - ISM Circular Distribution System, as of Q4 2024)

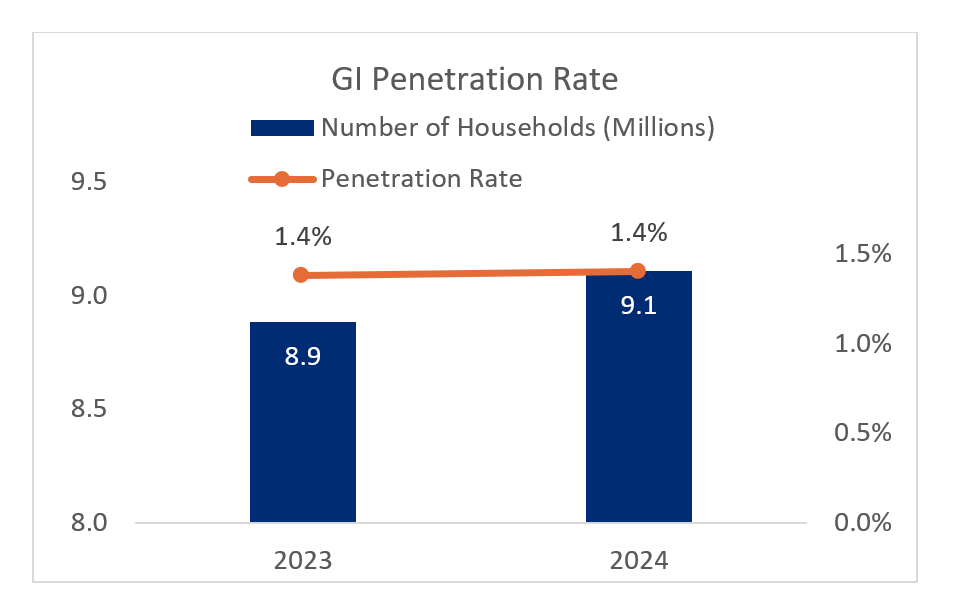

The relationship between increasing household numbers, shifting inflation, and Malaysia’s GITOs penetration rate reveals the extent of insurance coverage across the population in terms of accessibility and reach.

Malaysia’s residential development and household formation continued to expand in 2024, with 9.1 million households and 10.6 million living quarters recorded, compared to 8.9 million households and 10.4 million living quarters in 2023. Despite this growing population base, the GI penetration rate remained low at 1.4% in 2023. This data underscores a significant opportunity for the industry to broaden its reach and increase insurance adoption, particularly by enhancing awareness of personal insurance products. Addressing this gap is vital to strengthen financial protection for a greater number of Malaysian households nationwide.

(Source: Number of Households and Living Quarters – Malaysia’s Official Open Data Portal, as of Q4 2024; GWP - ISM Circular Distribution System, as of Q4 2024)

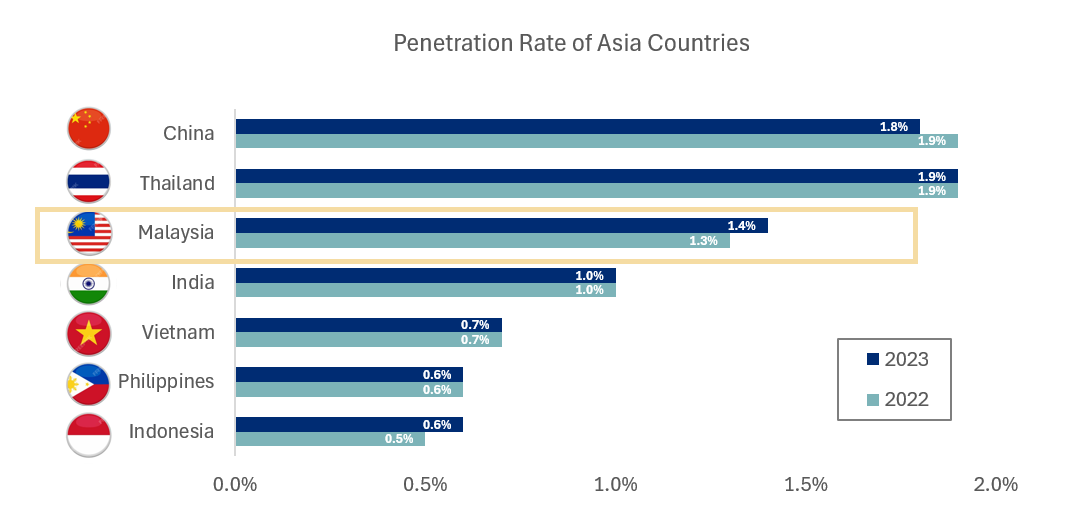

Comparative data positions Malaysia’s GITO penetration rate alongside key regional markets such as China, India, Indonesia, the Philippines, Thailand, and Vietnam. The benchmarking offers valuable insights into Malaysia’s standing within the broader Asian insurance landscape.

In 2023, Malaysia ranked third among these selected Asian markets, achieving a general insurance penetration rate of 1.4%, a positive step up from 1.3% in 2022.

While the growth may appear modest, it reflects steady progress in strengthening insurance adoption across the country. Malaysia’s position ahead of several regional peers highlights the relative maturity of its GI sector, while also pointing to untapped potential when benchmarked against higher-penetration markets like China. Continued efforts to boost awareness, affordability, and accessibility of insurance products remain key to driving further growth.

(Source: Penetration rate - Swiss Re Sigma 3/2024 Report & Swiss Re Sigma 3/2023 Report)

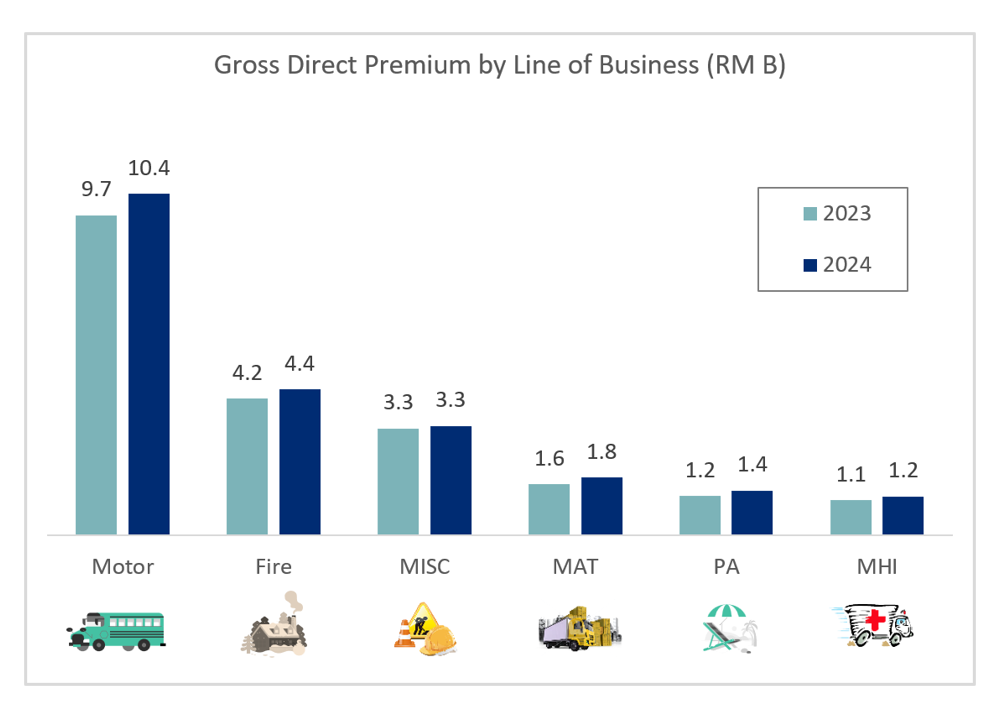

The general insurance industry’s premium distribution is split across 6 lines, including Motor, Fire, Medical and Health Insurance (MHI), Personal Accident (PA), Marine, Aviation and Transit (MAT) and Miscellaneous classes.

This breakdown highlights consumer demand and business coverage trends within Malaysia’s general insurance market.

In 2024, Malaysia’s general insurance industry recorded a 7.1% growth in Gross Direct Premium (GDP), reflecting continued demand across all lines. The Motor insurance class remained the dominant contributor, accounting for 46.2% of total GDP, followed by the Fire class at 19.7%. This composition underscores the importance of vehicle and property protection within the Malaysia market, driven by rising vehicle ownership and ongoing development in the residential and commercial sectors.

(Source: ISM Insurance Services Malaysia Berhad, data as of Q4 2024)

Further significant contributors came from Medical and Health (MHI) at 5.3%, Personal Accident (PA) at 6.1%, and Marine, Aviation and Transit (MAT) at 7.9%. The remaining 14.8% was made up of Miscellaneous classes. This diverse portfolio reflects the industry’s broad role in supporting personal and business risk protection needs, with Motor and Fire continuing to anchor overall growth.

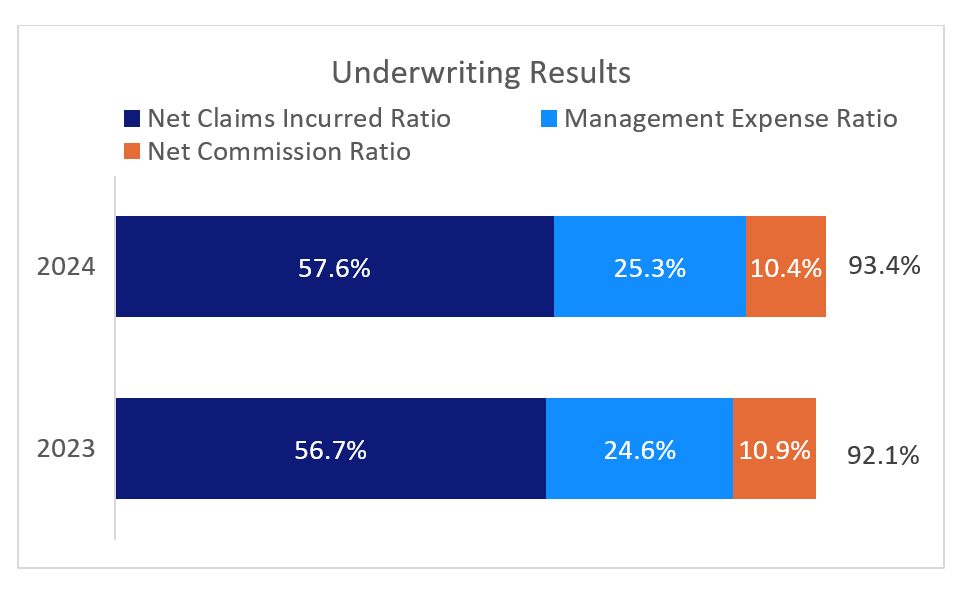

A closer look at general insurers’ underwriting results reveals key performance indicators such as Net Claims Incurred (NCI) Ratio, Commission Ratio, Management Expenses (ME) Ratio and the Combined Ratio (CoR). These metrics provide a comprehensive picture of industry profitability and operational efficiency.

Combined Ratio rose to 93.4% in 2024, primarily driven by a higher Net Claims Incurred Ratio (NCIR), which reached 57.6%. Notably, the Motor segment – a key contributor to overall claims activity – the NCIR climbed from 66.7% in 2023 to 68.6% in 2024, inching closer to pre-pandemic levels seen in 2019 (70.1%). This upward trend reflects growing claims frequency and cost, highlighting the ongoing need for careful portfolio management and pricing discipline across the general insurance industry.

(Source: ISM Insurance Services Malaysia Berhad, data as of Q4 2024)

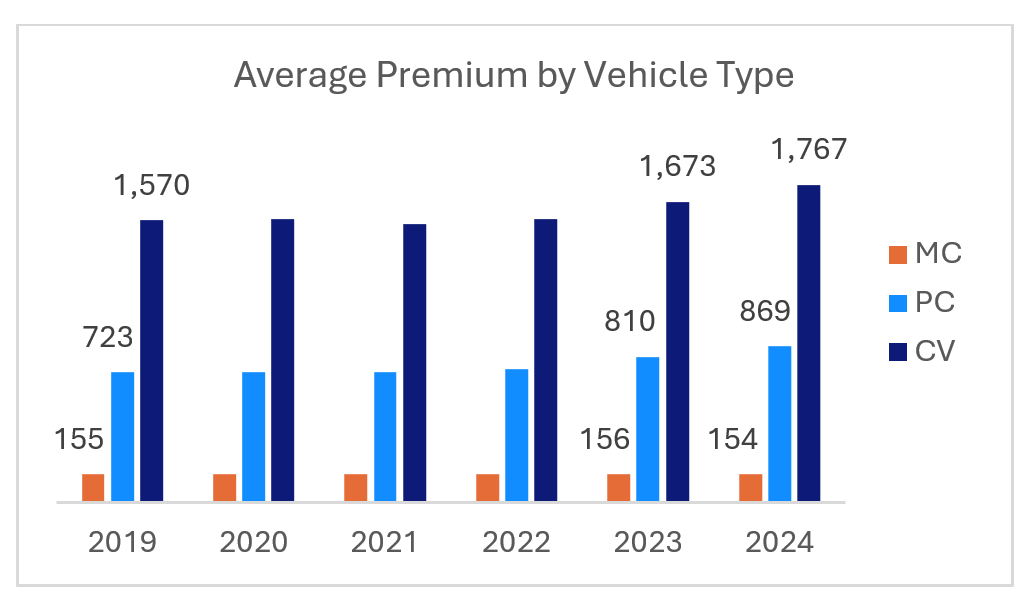

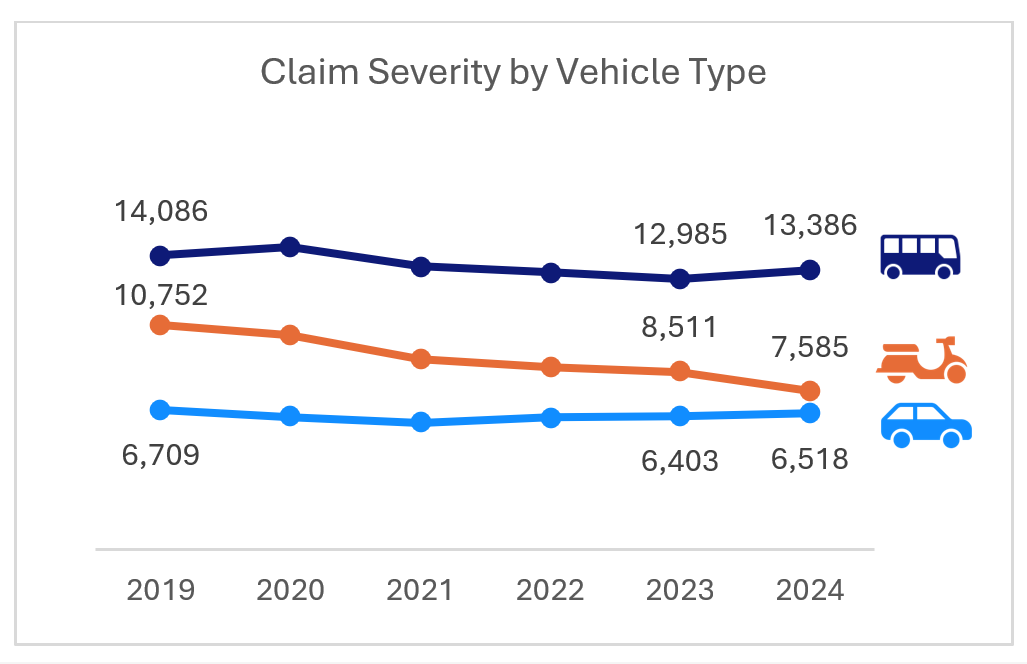

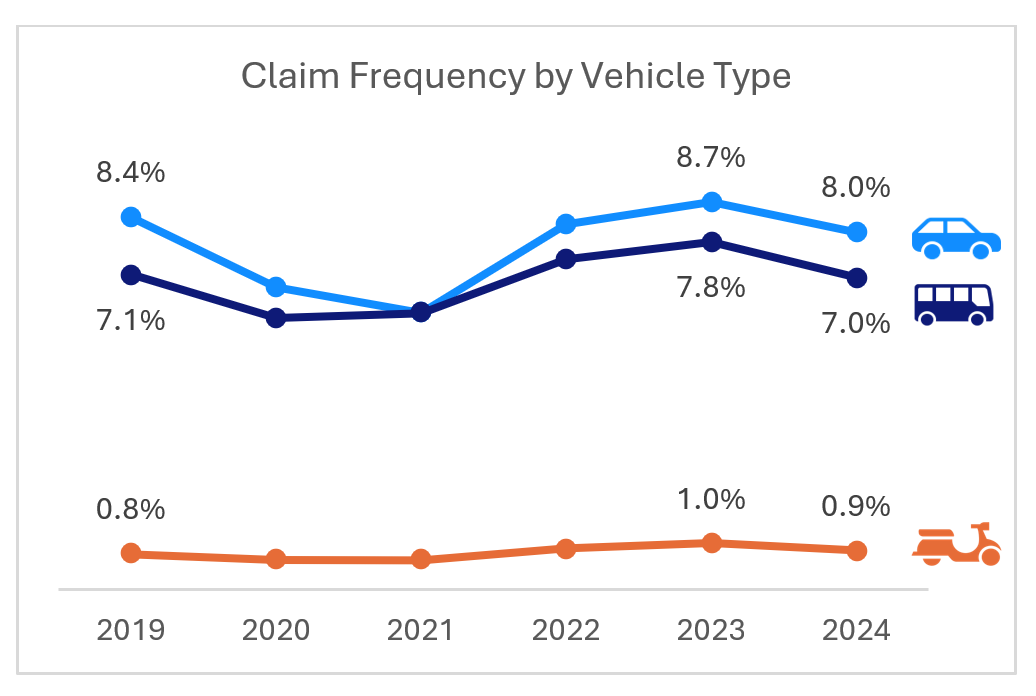

Motor Insurance for Private Cars (PC), Motorcycles (MC) and Commercial Vehicles (CV), a core component of the retail segment, shows evolving patterns in average premium, claim frequency, and claim severity.

The average premium trend offers insight into the cost of insuring different types of vehicles. CV consistently carries higher premiums due to its Sum Insured. MC premiums have remained relatively stable at around RM155. In contrast, the average premium of PC has shown an upward trend from RM723 in 2019 to RM869 in 2024, driven by escalating repair costs.

Claims severity reflects the cost of more serious road accidents, including major vehicle repairs or injuries sustained. Among all vehicle types, MC consistently show higher claim severity than private cars, due to the greater risk of serious injury or fatality. The claim severity has improved over time – decreasing from RM 10,752 in 2019 to RM 7,585 in 2024, remaining relatively manageable as parts become more readily available.

Claim frequency indicates the rate of accidents or losses. MC claim frequency is significantly lower because owners tend to purchase only basic or third-party coverage. The claims frequencies for both PC and CV remained manageable hovering around 7-8% yearly.

| Types of Products | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

| Fire (Material Damage) | 2,217 | 2,232 | 2,269 | 2,374 | 2,468 | 2,473 |

| Houseowner | 312 | 353 | 341 | 338 | 324 | 369 |

| Householder | 229 | 229 | 211 | 126 | 90 | 136 |

| Industrial All Risks (IAR) – Material Damage | 127,978 | 151,001 | 173,178 | 212,787 | 293,002 | 342,877 |

(Source: ISM Insurance Services Malaysia Berhad, data as of Q4 2024)

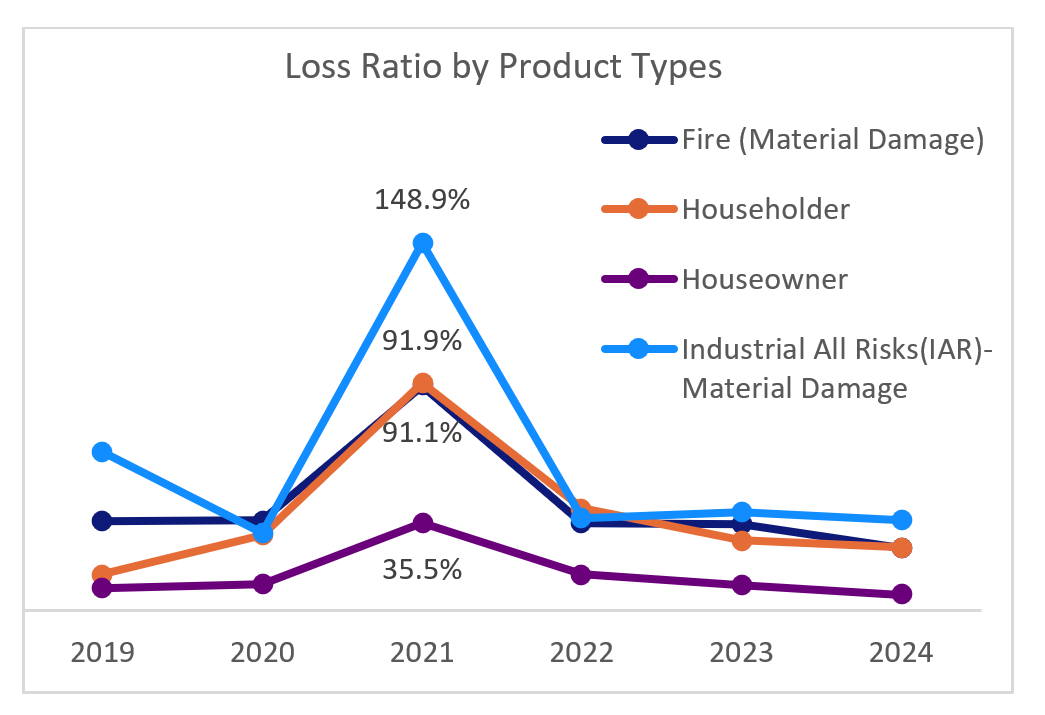

The average premium for fire insurance provides a clear understanding of the costs involved in protecting various types of property ranging from residential to commercial buildings and their contents. In recent years, average premium for Fire policies has been rising, driven by the increasing cost associated with safeguarding properties against risks such as fire, lighting, and other potential damages.

Loss Ratio is a crucial metric for assessing an insurer’s performance where a higher loss ratio indicates more claims payouts relative to collected premiums. In 2021, all four fire products experienced a significant increase in Loss ratios due to the Great Flood in Klang Valley.

(Source: ISM Insurance Services Malaysia Berhad, data as of Q4 2024)

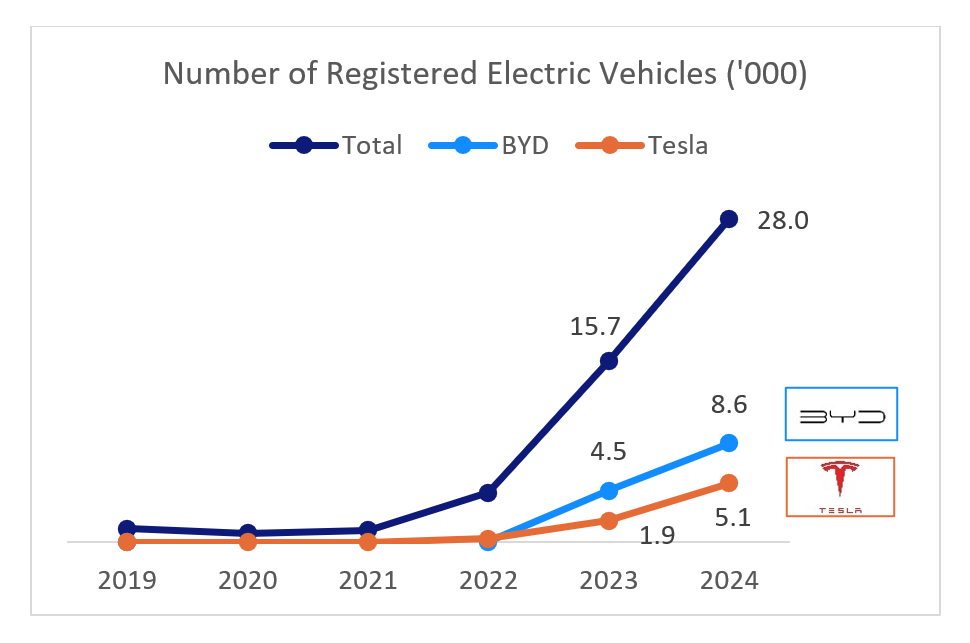

With the Government’s push for green mobility, the number of Electric Vehicles (EVs) registered in Malaysia has seen a significant growth. This data provides an indication of emerging insurance needs within this segment.

Malaysia’s electric vehicle (EV) landscape is rapidly expanding, with registrations surging by an impressive 79% growth - from 15,669 in 2023 to 28,048 in 2024. This rapid acceleration reflects growing consumer confidence, improved infrastructure, and stronger market offerings. Notably, the surge has been fueled by standout performances from key car manufacturers. BYD nearly doubled its registrations, jumping from 4,470 to 8,570 units, while Tesla saw a significant increase from 1,873 to 5,137 units. As more brands enter the market and consumer interest grows, the EV segment is quickly becoming a crucial area to monitor in Malaysia’s mobility and insurance sector.

(Source: Malaysia’s Official Open Data Portal, as of Apr. 2025)

This growing adoption of EV presents both exciting opportunities and new challenges for the general insurance industry. The introduction of advanced vehicle technologies requires insurers to adapt to changing risk profiles, evolving repair cost dynamics, and emerging coverage needs such as battery protection, software reliability, and Advanced Driver-Assistance Systems (ADAS). The rise in EV ownership clearly signals a need for innovation in product development and risk assessment, making this a particularly dynamic area within the motor insurance sector today.

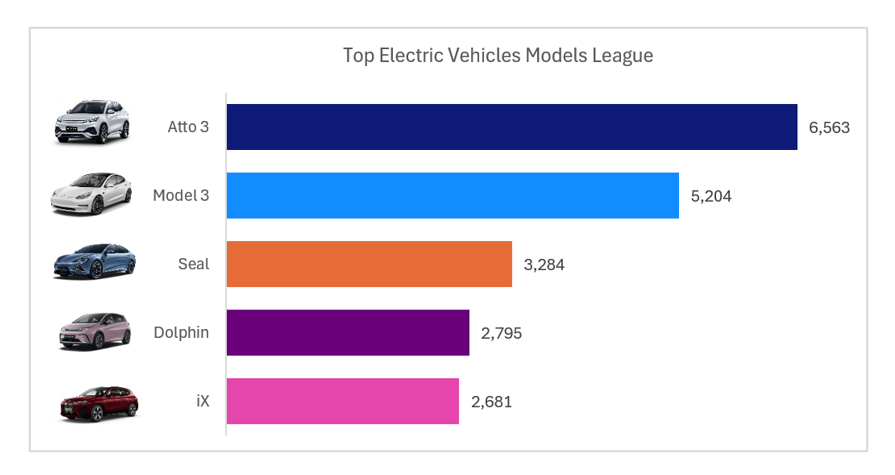

A snapshot of the most registered EV models in Malaysia, providing a clearer view of market preferences and potential coverage trends in the near future.

Malaysia’s electric vehicle (EV) market witnessed a remarkable growth in 2024, with several car models leading the charge.

Malaysia’s electric vehicle (EV) market witnessed remarkable growth since 2022, with several models leading the charge. The BYD Atto 3 emerged as the top-selling EV, registering 6,563 units, followed by the Tesla Model 3 with 5,204 units. BYD's offerings also made a significant impact, with the Seal recording 3,284 units and the Dolphin 2,795 units. The BMW iX rounded out the top five with 2,681 units registered.

(Source: Malaysia’s Official Open Data Portal – Vehicle Registrations, as of Q4 2024)

The Malaysian EV market is becoming increasingly dynamic, driven by factors such as competitive pricing, diverse model offerings, and supportive government policies. As the EV landscape evolves, these developments signal a promising trajectory for Malaysia's transition to sustainable mobility, offering consumers a broader range of choices and contributing to the nation's environmental goals.

Financial Year

12-month accounting period that a business uses for financial and tax reporting purposes.

Compound Annual Growth Rate

Annualized rate of return of a financial metric over a defined period.

Combined Ratio

Measures the profitability and financial health of an insurance company.

Combined Ratio

=

Net Claims Incurred+Net Commission+Management Expenses

Net Earned Premium

Gross Direct Premium

Total amount of premiums collected by direct insurance business without deduction for commission or brokerage.

Gross Written Premium

Total amount of premiums that an insurance company has charged for policies issued.

Management Expenses

Expenses incurred in the administration of an insurer which are not included for settling claims.

Net Claims Incurred

The total amount of claims paid is adjusted by the change in the claims provision.

Net Claims Incurred Ratio

Measures the proportion of claims incurred to earned premiums.

Net Claims Incurred Ratio

=

Net Claims Incurred

Net Earned Premium

Net Commission

Fee paid to an agent or broker as a percentage of the premium.

Net Earned Premium

Amount of premiums that an insurance company recognizes as earned revenue based on the time elapsed.

Penetration Rate

Indicates the level of development of insurance sector in a country.

Penetration Rate

=

Premium

Gross Domestic Product

Motor

Protects the individual against financial losses in the event of an accident involving private car, motorcycle, and commercial vehicle.

Fire

A type of property insurance that provides financial protection against losses caused by fire.

Personal Accident

Provides compensation in the event of injuries, disability or death caused solely by violent, accidental, external and visible events.

Medical and Health

Covers the cost of private medical treatment, such as the cost of hospitalization and healthcare services.

Marine, Aviation and Transit

Covers the loss of marine cargo, air cargo, land transit, marine hull, operation of aircraft and oil and gas exploration.

Miscellaneous

Refers to workmen’s compensation, liability insurance, bonds and other types of insurance not falling within any of the above classifications.